Financial Innovation where SA needs it most: The SmartWage story

James Lightbody

James Lightbody

The blue-collar employment market has always had a major issue around the world. This issue is best described as liquidity. Wages are paid once a month while humans consume every day, meaning expenses accrue daily – problem. There is a mismatch in cash between a monthly inflow and daily outflow. The result is payday loans, high-interest rates and debt traps, none of which are a good time for the individual or society as a whole. SmartWage, a new startup, believe they have cracked the code in this previously intractable problem. How do you ask? A joint attack of distributing a portion of wages mid-month (for a small fee), with the barrier to releasing this money in the form of financial education. It’s a clever solution of shifting credit risk from employee to employer, drastically reducing costs in the system.

SmartWage was founded by Simon Ellis, Alex Platt and Nick Platt in late 2019 when they saw a similar company in the UK, Wagestream, solving the problem of wage liquidity (a big enough problem in the UK and Europe that the company recently raised a $51m series A). Concerned with financial education being a barrier to growth in a large portion of the South African population, the SmartWage team took a closer look at the issue in South Africa to see if an adapted version of Wagestream could be effective in solving it.

Understanding the problem

To expand on the issue that I alluded to in the introduction, the major factors boil down to liquidity and time preference. Wages are paid once a month. Required expenditure, being food and other necessities, accrue daily. This creates a liquidity imbalance for everyone who earns monthly (the vast majority of the population). The solution to this problem is financial planning. You need to keep a portion of your monthly salary aside for the food bill of day 30 of the month. This may be easy when your wage provides a large amount of disposable income, but if you earn anywhere near to the bread line, this requires detailed planning as well as avoiding the second problem of time preference bias.

There is an unnecessarily complicated term from economics (classic!) called hyperbolic discounting. It describes the very human phenomenon of finding the same product more attractive today than it is tomorrow. On average, people would rather have one treat today, than two tomorrow (but are happy to wait for two treats a year and one day from now over one treat a year from now – the effect is non-linear). Hyperbolic discounting is important in this context as it makes the budgeting process even more difficult. Some have argued it’s against human nature. Faced with the opportunity to spend our wages on immediate gratification at the beginning of the month vs saving for a rainy day, we mostly pick the former.

The solution to date

So how has this problem traditionally been solved in South Africa? Government and support agencies attempt to solve the gratification part with education around financial planning, while the market solves the liquidity with high-interest loans. The education part is really up against it due to the human nature element they are trying to crack. Without rewards to override the immediate gratification, it is unlikely to be effective (and hasn’t been to date). On the liquidity side, when I say this is provided by the market, I mean the black market. The loan market is regulated for good reason. It becomes unprofitable for banks to lend to parties with such a high credit risk (low-income earners with no assets) if the amount of interest they can charge is capped. This void is either filled by employers (if they have liquidity and motivation) providing advances on employees’ salaries or by the black market, providing loans at interest rates that banks aren’t allowed to (they also employ collection methods that banks aren’t allowed to, making it a viable, albeit illegal business).

The SmartWage solutionn

As a result, the problem looked intractable and is the space that SmartWage waded into. Their approach is certainly novel and involves two key differences in how the problem was solved before.

- Link the solution of liquidity (wage advance) and immediate gratification (education) into one product as opposed to treating them separately; and

- Change the credit risk from employee to the employer while keeping the liquidity, cost and admin overhead away from the employer.

So how does it work? Simply put, SmartWage will pay out a portion of employees’ wages mid-month for a fee. The payment is conditional on the employee completing financial education exercises through Facebook Messenger. The balance of the wages are paid to employees at the end of the month net of the fee SmartWage takes, and SmartWage is reimbursed by the employer. The credit risk is thus on the employer and not the employee (given that the fee is paid directly from the cash flow of the employer). Employees pay a smaller fee for liquidity (3-5% vs 15% on the black market) while receiving free financial education. Employers aren’t charged and society as a whole benefit from a more educated and less indebted populous. The only unhappy parties are the black-market lenders, which are being outcompeted. Not tragic. It’s a rare win-win-win scenario.

There are others who tried a similar solution in South Africa but tended to do the education element through a downloadable application. A forced application download created the benefit of allowing more creative and deeper education content, but at the same time created the joint hurdle of requiring a smartphone and an app download. A large portion of the target market (low earning blue-collar workers) do not have smartphones, making this solution a non-solution. SmartWage opted to do the financial education through Facebook messenger (and communication through USSD, SMS and WhatsApp). This removes the need for an app download and provides a workable solution. Sure, an element of flexibility on the financial education front is lost, but it’s a small price to pay to get the product going.

And get going it has. Since official launch, in February 2020 the uptake has been pretty phenomenal. In the first 3 months (to May), there are already 24 employers using their platform – clearly a big need for the offering in the market. The lockdown implemented in South Africa in late March had many consequences, one of which was a huge liquidity strain on workers. SmartWage was not only able to step in and assist a lot of businesses with getting liquidity to their workers. They also waived the fee for April-June to make the solution a no-brainer for workers while developing a large client base for fees that switch back on in July – smart. There is nothing sinister about this – it is a version of the freemium business model very commonly used to get users using a version of your product with as little a hurdle as possible. Instead of creating a free tier, SmartWage has used a grace period.

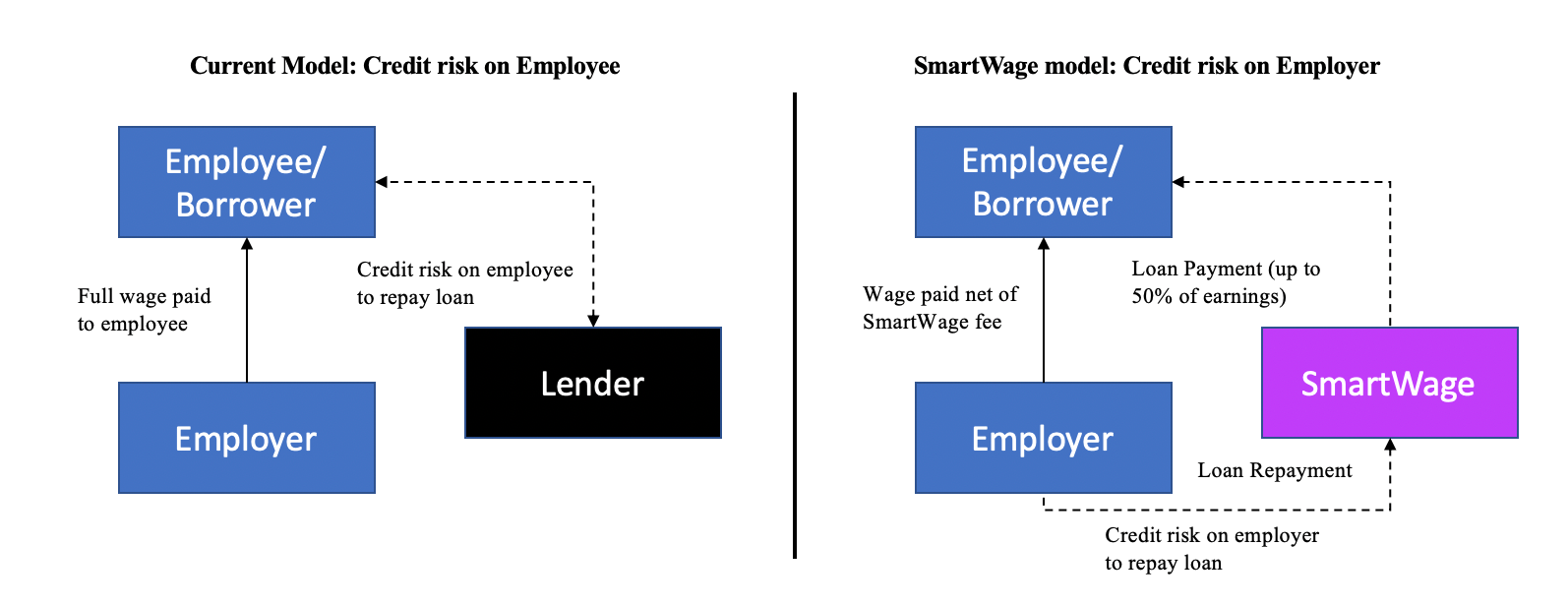

An obvious question is how SmartWage can charge so much less than the black market? Most people know the concept of a personal credit score. Higher credit score = more access to credit at lower rates. Credit score too low means no loans whatsoever. Employees with no savings and low wages fall into the low credit score bracket. SmartWage have sidestepped this problem by paying out employees’ wages based on the payment to come by employers (illustrated in figure 1). What this does is shift the credit risk from individual employees (with no credit record) to employers. Employers have a better ability to borrow money short term and thus can be lent to at a lower interest rate.

Credit risk with SmartWage

Figure 1: Credit Risk Transfer

Figure 1: Credit Risk Transfer

Why don’t employers do it themselves? Employers have businesses to run and don’t want to play bank for their employees. Having the admin and liquidity hurdle taken by someone else is highly preferable. SmartWage though IS playing bank and thus needs a lot of liquidity to make these short-term loans (especially as they grow). For example, if they have 20,000 employees each earning R6,000 per month and requesting 50% of their earned salary halfway through the month, the short-term liquidity requirement is R30m. 200,000 clients – R300m. The number gets big. Given SmartWage’s exposure being widely diversified across corporate SA, this risk is palatable as a whole to a bank (or will be in time). At maturity, I’d guess SmartWage should be able to borrow at Prime + 4% (12.75% as of writing). The low end of their fee range (3%) for 15 days lending equates to an effective annual interest rate of 73% (industry method of calculation used). Even if you build in a default rate of 10%, that’s good business. I’d guess their capital raising is going well (currently raising R20m debt in the near term and a further R80m in the next 6 months).

For the purposes of this analysis, I’m assuming that SmartWage is above board in their approach. They have a legal opinion that they don’t need to be registered as a financial services provider (they’re also engaging with the relevant authorities on this) and while it’s important to note as regulatory risk, I don’t have the expertise to comment on it. Other risks that are worth noting are the employer defaulting on salary payments and employees being laid off before the end of the month (so advanced earnings not fully earned). The first risk of non-payment is covered 90% by insurance according to SmartWage. I’d guess the price of covering this risk has gone up since COVID-19, but as they grow a portfolio of employers, I’d think this cost would go down on a relative basis. The risk of employees getting laid off early is removed by the early wage payment being capped at below what the employee has worked. i.e. if fired on day 20 of the month, only 50% of their earned wage would have been paid, making this a non-risk.

They’re young, but where to?

I can never resist the speculation train, especially for companies that have the potential of locking in a large distribution channel like SmartWage do (not difficult to see them providing loans for over a million people within a few years). The loan business is of course very large. Currently, their average transaction size is just under R1,500. If I use that rounded figure and assume 1 million users use their product every second month, that generates R270m a year of revenue – a great business opportunity (on conservative assumptions). Assuming they can secure debt at 2x equity at maturity, it’s close to a 100% ROC business. There is no reason to think that the average loan size may not increase over time as well. Their focus, for now, is of course on getting this product right. I don’t see their technology as a major barrier to entry (by design it is quite simple) and they will need to move quickly to capture a large part of the market before copy cats move in. In this regard, they certainly seem to have the right level of urgency, focusing on partnerships to aid their distribution (Clanstival and Yoco two notable ones that were recently announced). Their offering of 0% fee for April – June will also build fast distribution and trust with employers (who gate access to their employees).

As I’ve said before, the name of the game with a new startup is the focus. As Patrick Collison from Stripe has said many times, take the lake before you take the ocean. Once they have the lake, the ocean of other products will await them (from all kinds of insurance, banking and other loan products – just please not another funeral policy). They will also generate all kinds of interesting data on consumer habits and how it changes with the intervention they provide. This will be fascinating both from a government policy intervention perspective as well as SmartWage’s potential product line. Winning the initial advantage is all that really matters at this stage and seems to be exactly what they are focusing on.